All Bharat Bond ETF: A Secure, High-Yielding Investment 💰

Bharat Bond ETF is India's newest investment opportunity in the secure space. Read this blog to know everything Bharat Bond ETF

Bharat Bond ETF invests in Public-Sector companies' Bonds

This can be your VERY SAFE alternate to FDs, PPF etc.🤯

Here's everything you need to know about Bharat Bond ETF👇

1. What is an ETF?

Exchange Traded Funds (ETF) are type of mutual funds which are listed and traded on exchange.

These ETFs track an underlying index and are passively managed.

An ETF can consist debt (think, loan) as well as equity instruments.

The Bharat Bond ETF consists of debt securities (bonds / debentures) whereas, a Nifty 50 Index Fund or Nifty BeeS fund consists of equity instruments.

2. What is Bharat Bond ETF?

Think of Bharat Bond ETF like just any other Debt Mutual Fund which invests in debt securities of companies. Such debt securities are often called debentures or even bond as well.

However, there are certain differences which make Bharat Bond ETF different from any other Debt Mutual Fund

The Bharat Bond ETF is a Debt Mutual Fund which invests in BONDS:

Of Govt-owned entities having AAA-rating

Having a target maturity

Another difference is that the Bharat Bond ETF doesn’t pay regular coupon or interest payments on bonds which some Debt Mutual Funds give

The investor

The latest issue will invest in govt companies' bonds maturing in April, 2033

Does this mean I can't get the money invested till Apr, 2033? Read👇

No.

Liquidity and lock-in conditions

An ETF is freely tradable on exchanges.

This means that even though the bonds will pay you back money in April, 2033

Just like you sell stocks, You can sell these bonds to an investor on the exchanges who wants it from you

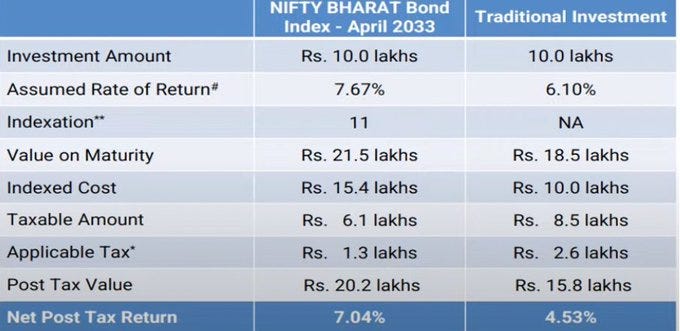

What about Returns?

The present day return (YTM) on these public sector bonds is ~7.67%

Your expected returns can be around the same A comparison between Bharat

Bond ETF and FD (at 6.1% interest rate) has been made by Edelweiss AMC

Are the returns guaranteed?

Just like the debt funds, the value of a debt fund moves up and down with the change in interest rates

So, if interest rates --> Go up, value of bonds goes down --> Go down, value of bonds goes up In PPF, FD etc. this risk isn't there

What about costs?

The Bharat Bond ETF comes with lowest possible expense ratio of just 0.0005% 🤩

This is where it beats Debt Mutual Funds having 0.2-0.5% expense ratios

You are getting almost all the interest that these companies are declaring

Will I have regular income?

No. Unlike FDs, regular coupon payment bonds, Bharat Bond ETF pays at the end of maturity

But this is rather beneficial from two perspectives:

- Taxation (taxed at just 20% after Indexation)

- Compounding (because you won't withdraw interest)

What about risks?

A. Interest Rate Cycle - As explained in 4/, if interest rates go up, your return might suffer but the chance of principal value of bonds going down is less.

B. Default by entities - The chance of public sector entities default is damn low

Who is managing my money?

Bharat Bond ETF is a govt-led initiative only

The bid to run it was won by Edelweiss AMC Govt launched this initiative because to

issue bonds or seek for loans from banks came with a heavy cost

This was a win-win for both public and govt entities

—————————————————

Like this content? Share this with your friends and family members

—————————————————

You can learn more about Mutual Funds with out Mutual Funds club

—————————————————

Check out our courses on Basics of Stock Markets, Fundamental Analysis, Mutual Funds, Personal Finance and Value Investing

—————————————————

Thanks for reading :)

Disclaimer: Not investment advice. Kindly refer your SEBI registered Investment Adviser before taking any investment decision

Image source: Edelweiss AMC

Suppose I buy Bharat Bond ETF maturing in April 2032 in the secondary market via my broker Zerodha, will I be eligible for its fixed return if I hold it till its maturity date of April 2032 and secondly, is there any investment limit if I buy it in the secondary market? Thanks in advance.

Good read thanks for sharing.